Teaching your child how to handle money responsibly is an important lesson for parents to pass along. Did you know that it is also possible to pass along the gift of a strong credit score? I’ve heard that it was possible, but as our daughter just turned 18 recently, I wanted to find out personally. As they say, “be the data point you want to see”.

This story started several years ago. We wanted our teenage kids to have a card to use if they were out in case of emergencies, and planning to test out this approach both my wife and I added our daughter as an authorized user on accounts we have had open for some time and importantly, did not plan on closing any time soon. In our experience it was not possible with Amex, as you needed to share the authorized user’s social security number and they needed to be 18 already, but with CapitalOne and Chase, it was easy.

Why this matters

There are several components to a credit score, but the 2 largest by far (about 65% combined) are payment history and utilization. Of lower importance (15%) but relevant here is length of credit history. By becoming an authorized user on our accounts, we expected she would piggyback the benefits of a consistent payment history, very low utilization since those cards have a high available credit amount, and from accounts that had been open for over 5 years in each case.

With more use cases beyond rates for home or car loans depending on credit scores these days (insurance, renting, job search, etc), we wanted to give any potential boost possible. According to this SoFi article, the average credit score for an 18 year old was 681, which is higher than I expected. Can we do better?

The results

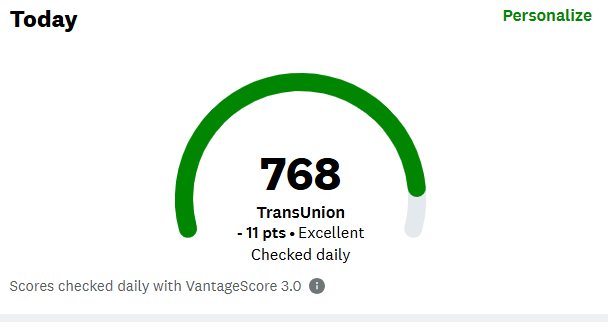

Our first check was via Credit Karma, which can see your Transunion and Equifax scores. There was no score yet for Equifax, but we were presently surprised to see a Transunion score of 779! That has since dropped to 768 after a new inquiry (more on that below), still great and also temporary until that new inquiry drops off.

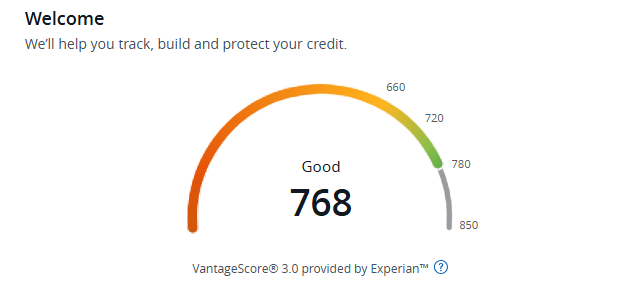

Next was Experian which ended up with a matching 768 score. While it’s great to see our strategy working in real life, a high score isn’t very useful until you try to use it. The final and most important experiment was to apply for a new credit card.

Our next experiment

While we weren’t going to go crazy and apply for a premium card which requires much higher minimum credit lines to approve, we didn’t want to go for a secured card or something like the Chase Slate which is made for people just trying to build their credit.

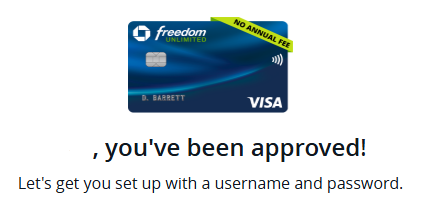

For us, the perfect option was the Chase Freedom Unlimited. Why? It has no annual fee so it makes a good long term keeper for her, it has an elevated $250 welcome bonus (or 25k Ultimate Rewards points if combined with a UR earning card) and there is also currently an elevated offer at Rakuten for an additional $75 back (or 7500 Bilt or Amex points). That was a nice combo to forgo a referral as we didn’t want that to somehow influence the approval odds.

As a Visa Signature card, it requires a minimum $500 credit line for approval, and even with her modest part time job income, she was instantly approved with said $500 of credit. After she shows a few months of responsible use, she will request a credit line increase which would reduce her utilization ratio and further build her credit score over time.

TL;DR: By adding our teenage daughter as an authorized user on long-standing Chase and CapitalOne accounts years ago, we successfully “gifted” her a 779 credit score on her 18th birthday. This piggybacking strategy bypassed the need for a secured card, allowing her to be instantly approved for her own Chase Freedom Unlimited with a $500 limit—proving that parents can jumpstart their children’s financial futures leveraging their own responsible credit history.